Navigation

SUBSIDIARY BOOKS – CASH BOOK

1. Meaning of Cash Book

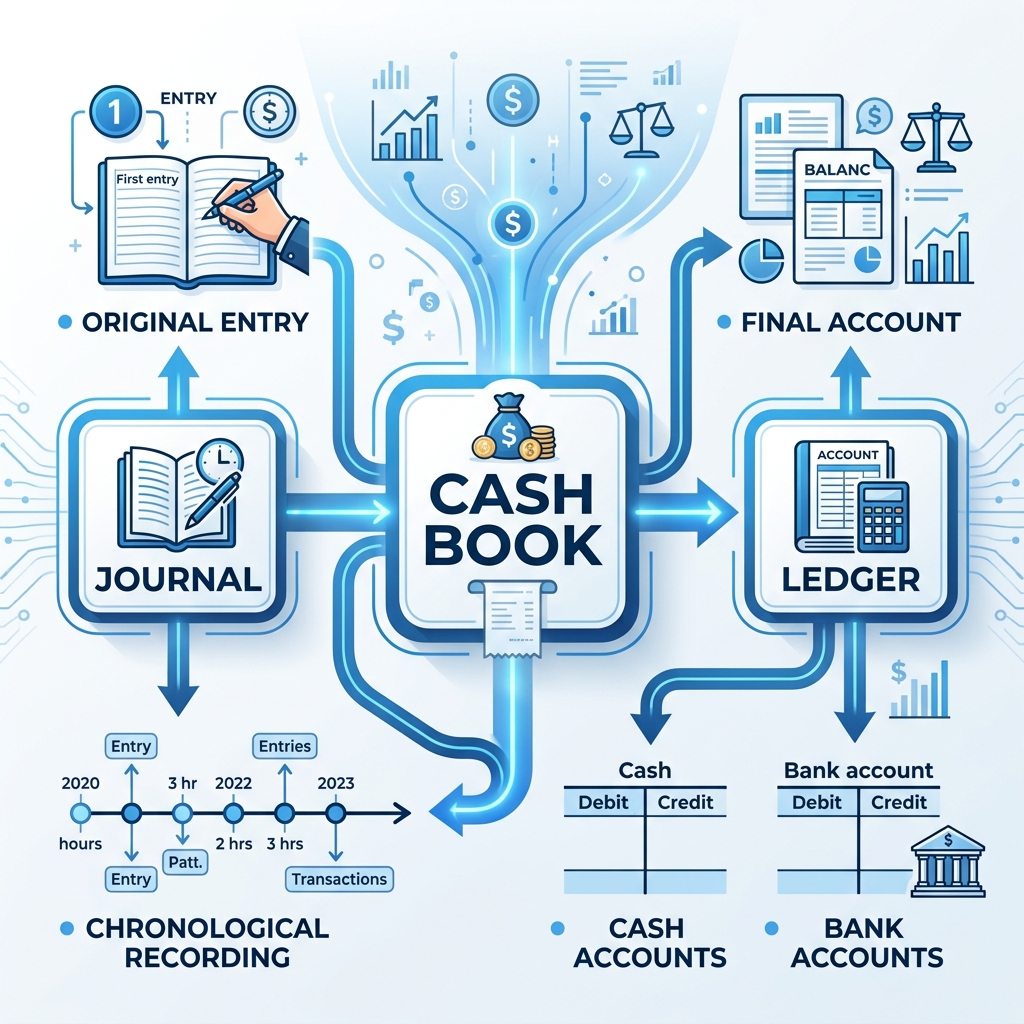

The Cash Book is a subsidiary book of original entry that records all cash receipts and cash payments in chronological order. It is the most important subsidiary book because cash is the lifeblood of any business.

Unlike other subsidiary books, the Cash Book serves a dual purpose:

- As a Journal: It is a book of prime entry where transactions are first recorded.

- As a Ledger: It contains the Cash Account and the Bank Account. Therefore, no separate Cash Account or Bank Account is maintained in the general ledger.

[!NOTE]

Definition (Carter): “Cash book is a book of original entry in which all cash transactions are recorded in a chronological order, and from which entries are posted to the ledger.”

2. Features of Cash Book

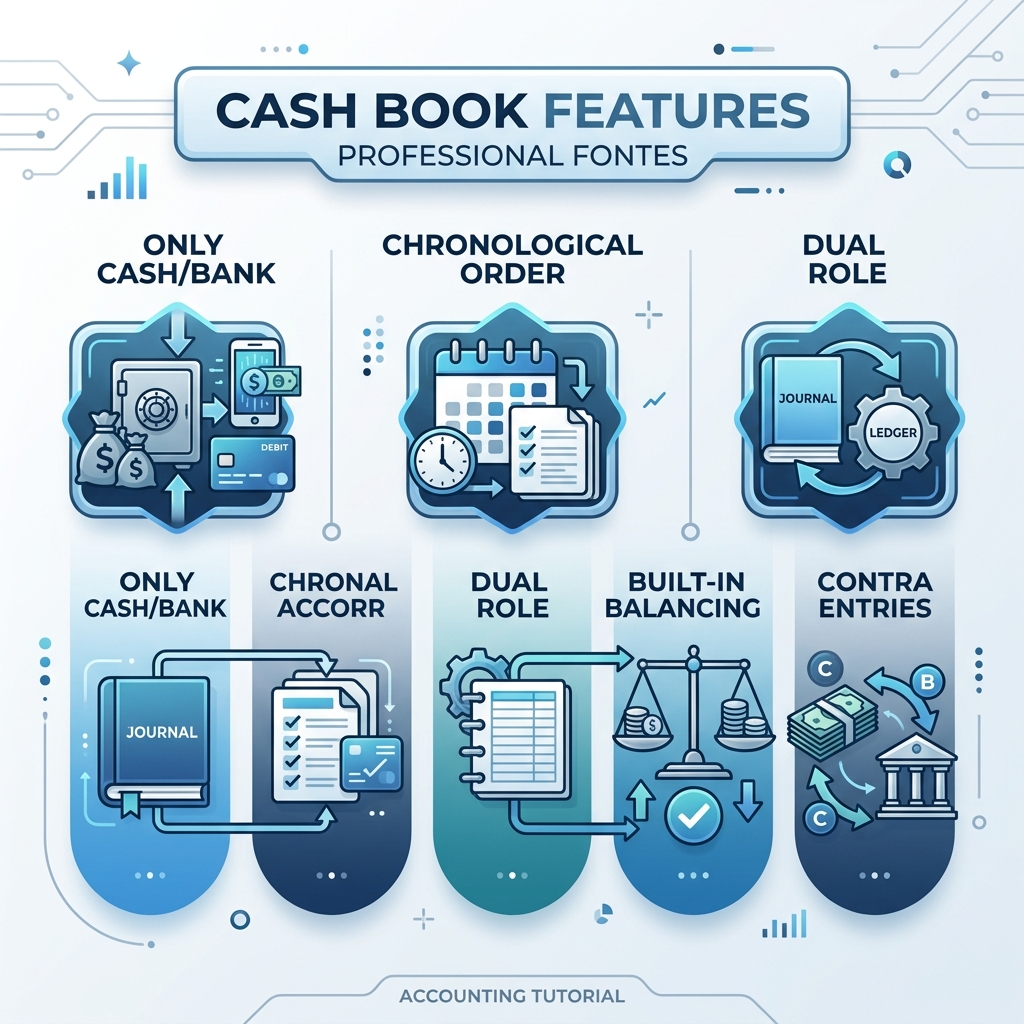

- Only Cash & Bank Transactions: It records only transactions involving physical cash or bank (cheques, deposits, withdrawals). Credit transactions (sales on credit, purchases on credit) are not recorded here.

- Chronological Order: Entries are made date‑wise, just like a journal.

- Dual Role: It acts as both a journal and a ledger.

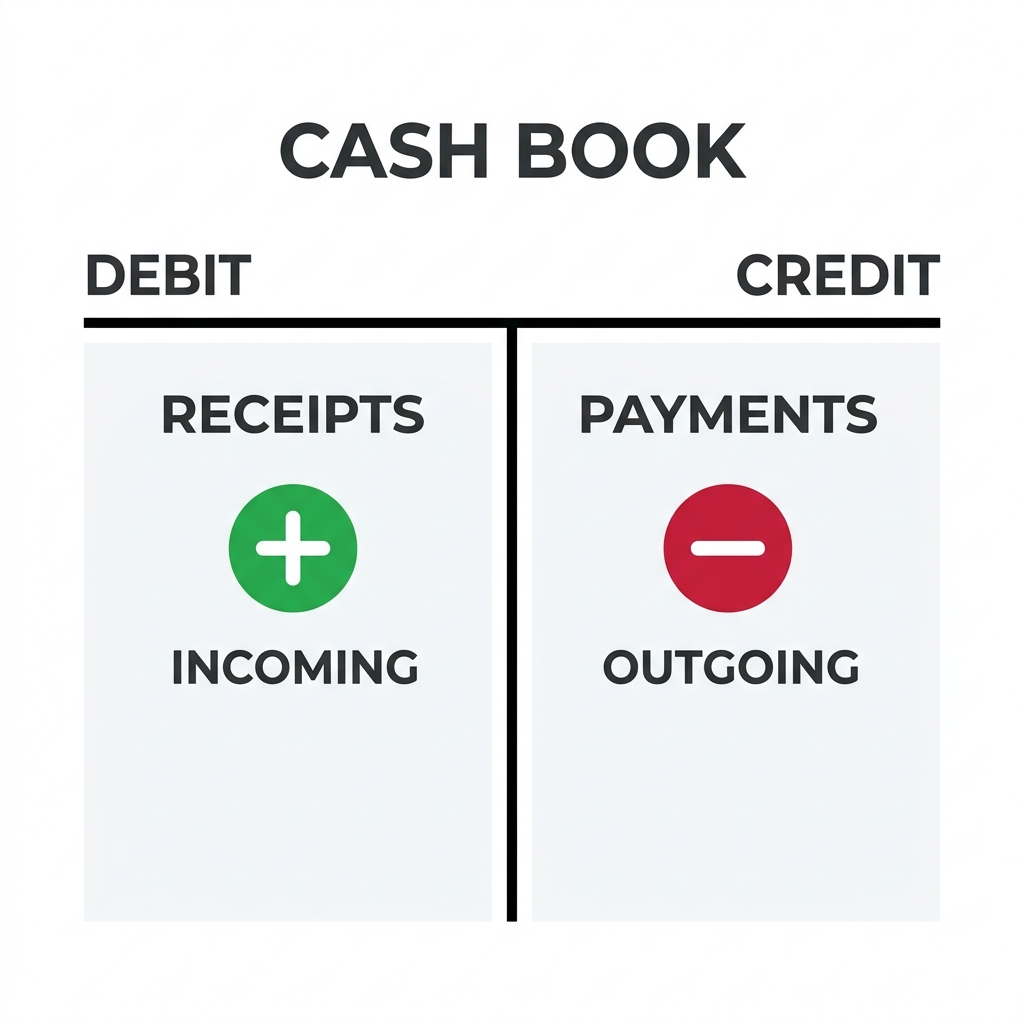

- Debit and Credit Sides: Receipts are recorded on the left (debit) side; payments on the right (credit) side.

- Built‑in Balancing: The cash and bank columns are balanced regularly (daily, weekly, or monthly) to show the actual cash‑in‑hand and bank balance.

- No Narration: Since the nature of the transaction is evident from the column headings and details, narrations are generally omitted.

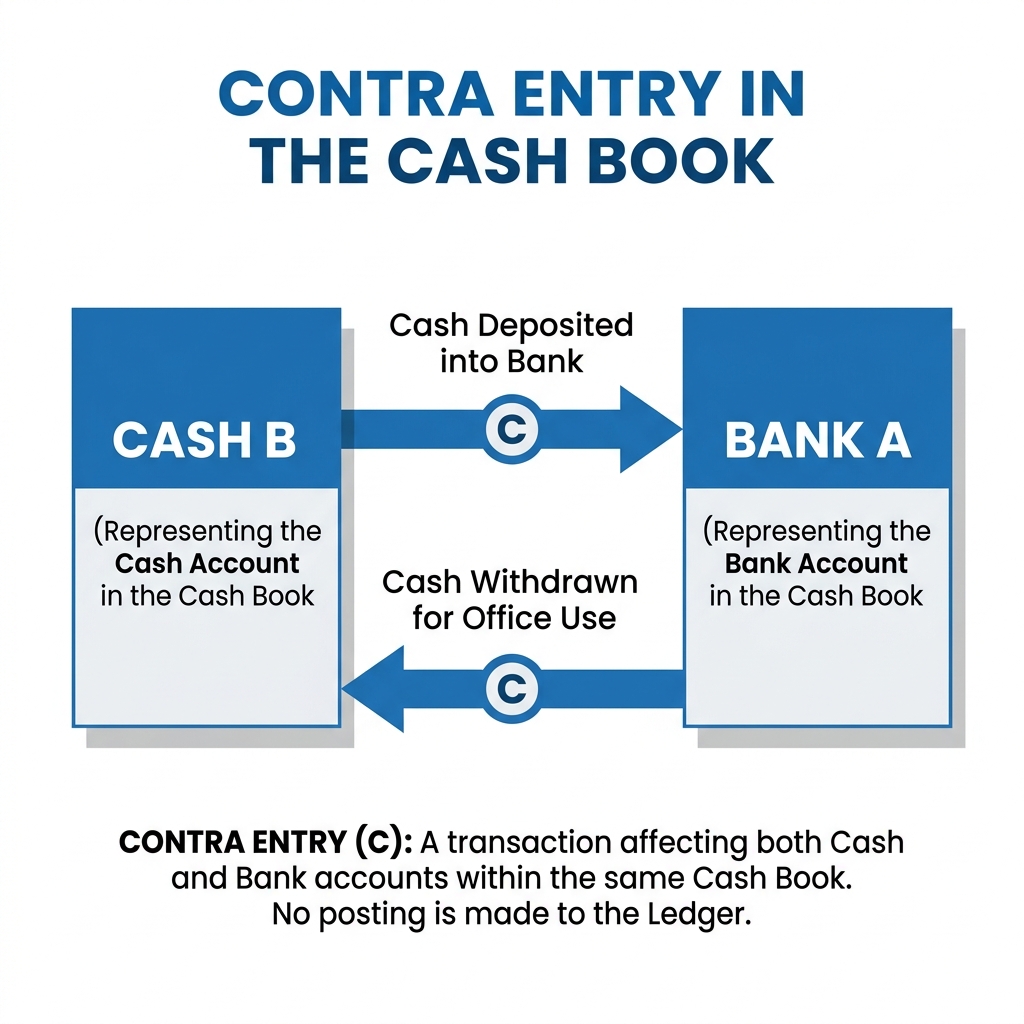

- Contra Entries: When a transaction affects both cash and bank (e.g., cash deposited into bank), it is recorded on both sides and marked with ‘C’ to indicate that no further posting is needed.

3. Advantages of Cash Book

| Advantage | Explanation |

|---|---|

| Instant Balance | The cashier can tell at any moment how much cash is in hand and what the bank balance is. |

| Saves Labour | No separate cash account is needed in the ledger, and posting from a separate journal is avoided. |

| Prevents Errors and Frauds | Daily balancing forces the cashier to account for all cash; discrepancies are detected early. |

| Helps in Bank Reconciliation | The bank column provides a clear record to match with the bank statement. |

| Efficient Division of Work | The cashier handles the cash book, while other clerks handle other subsidiary books. |

| Improves Internal Control | Because the cash book is constantly monitored, unauthorized use of cash is minimised. |

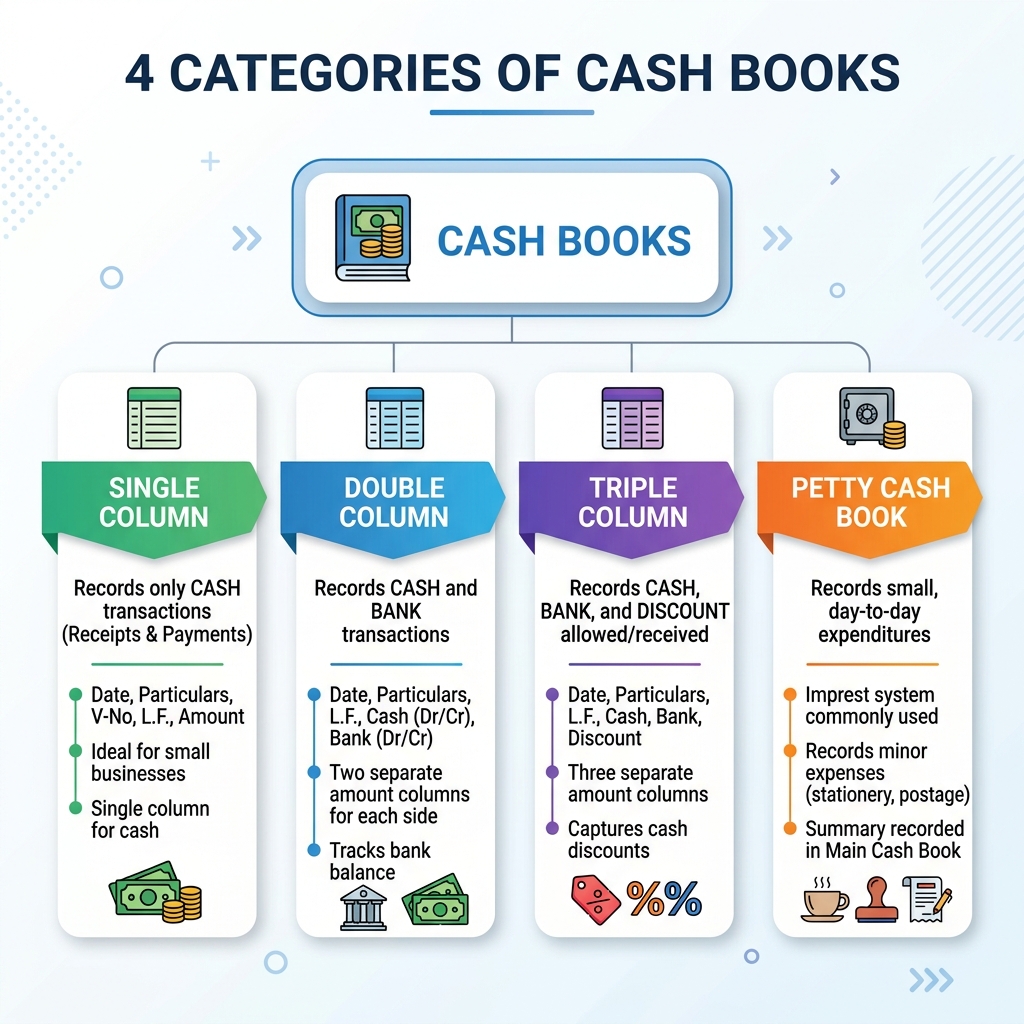

4. Types of Cash Books

Depending on the size and complexity of the business, the Cash Book can be maintained in four forms:

- Single Column Cash Book: Records only cash receipts and payments.

- Double Column Cash Book: Records cash and bank transactions; may also have a discount column.

- Triple Column Cash Book: Records cash, bank, and discount in one book.

- Petty Cash Book: Records small, repetitive expenses.

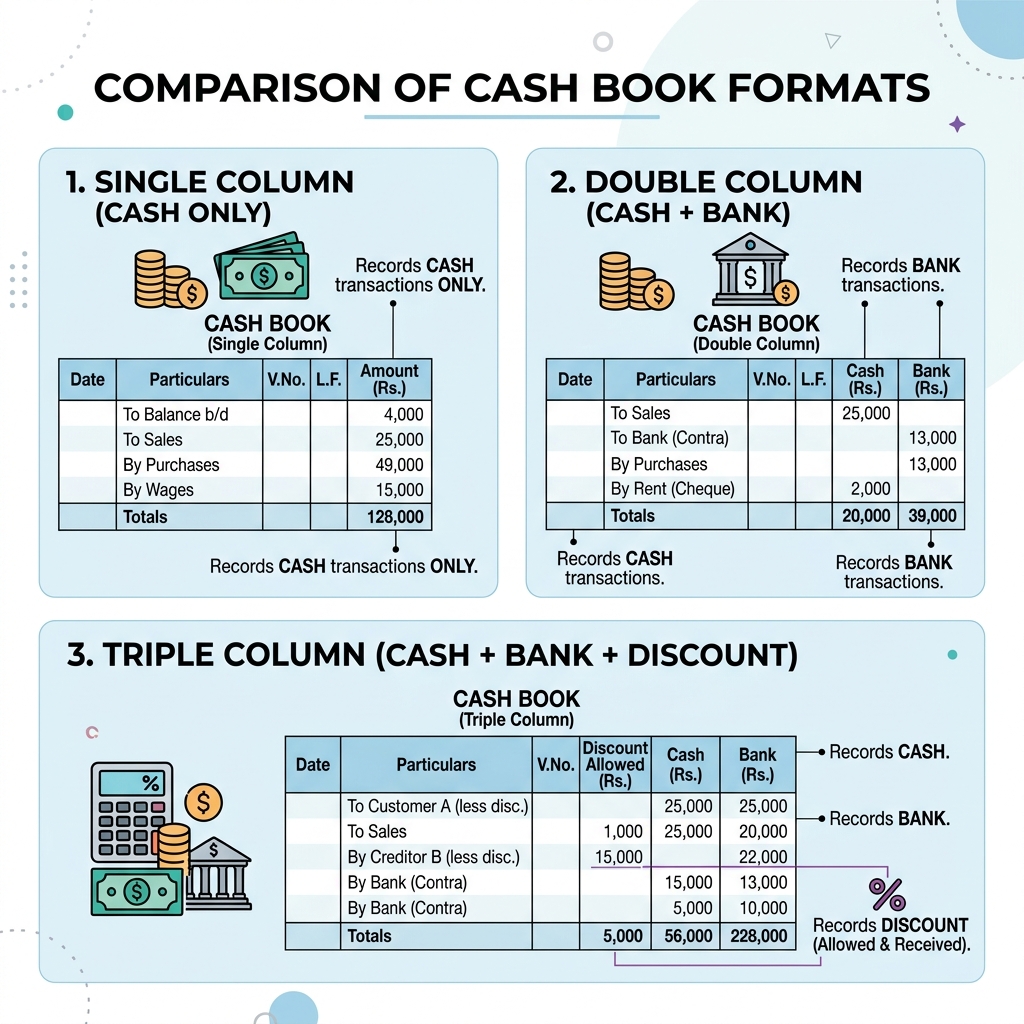

4.1 Single Column Cash Book

This is the simplest form. It has only one amount column on each side – the Cash column. It is used by small businesses that do not have a bank account or have very few banking transactions.

Format:

| Date | Particulars | L.F. | Amount (₹) | Date | Particulars | L.F. | Amount (₹) |

|---|---|---|---|---|---|---|---|

| To Balance b/d | xxx | By …………. | xxx | ||||

| To …………. | xxx | By …………. | xxx | ||||

| By Balance c/d | xxx | ||||||

| Total | xxx | Total | xxx |

Rules for Recording:

- All cash receipts are entered on the debit side.

- All cash payments are entered on the credit side.

- The cash column is balanced at the end of the period; the balance is carried forward as “To Balance b/d” on the debit side of the next period.

Illustration (Single Column Cash Book)

Problem: Enter the following transactions in a Single Column Cash Book:

- Jan 1: Started business with cash ₹ 50,000

- Jan 3: Purchased goods for cash ₹ 10,000

- Jan 5: Sold goods for cash ₹ 15,000

- Jan 8: Paid rent ₹ 2,000

- Jan 10: Received commission ₹ 500

Solution:

| Date | Particulars | L.F. | Amount (₹) | Date | Particulars | L.F. | Amount (₹) |

|---|---|---|---|---|---|---|---|

| Jan 1 | To Capital A/c | 50,000 | Jan 3 | By Purchases A/c | 10,000 | ||

| Jan 5 | To Sales A/c | 15,000 | Jan 8 | By Rent A/c | 2,000 | ||

| Jan 10 | To Commission A/c | 500 | Jan 31 | By Balance c/d | 53,500 | ||

| Total | 65,500 | Total | 65,500 | ||||

| Feb 1 | To Balance b/d | 53,500 |

4.2 Double Column Cash Book

The Double Column Cash Book has two amount columns on each side. The most common combination is Cash & Bank. It is used by businesses that frequently deal with cheques, deposits, and withdrawals.

Format (Cash & Bank):

| Date | Particulars | L.F. | Cash (₹) | Bank (₹) | Date | Particulars | L.F. | Cash (₹) | Bank (₹) |

|---|---|---|---|---|---|---|---|---|---|

| To Balance b/d | xxx | xxx | By …………. | xxx | xxx | ||||

| To …………. | xxx | xxx | By …………. | xxx | xxx | ||||

| By Balance c/d | xxx | xxx | |||||||

| Total | xxx | xxx | Total | xxx | xxx |

Important Rules:

- Receipts: Cash receipts go in the Cash column (debit side); cheques received go in the Bank column (debit side).

- Payments: Cash payments go in the Cash column (credit side); cheque payments go in the Bank column (credit side).

- Contra Entries:

- Cash deposited into bank: Debit Bank column (To Cash A/c) and Credit Cash column (By Bank A/c) – mark ‘C’ in L.F.

- Cash withdrawn from bank for office use: Debit Cash column (To Bank A/c) and Credit Bank column (By Cash A/c) – mark ‘C’ in L.F.

- Contra entries are not posted to any other ledger account.

Illustration (Double Column Cash Book – Cash & Bank)

Problem: Record the following transactions in a Double Column Cash Book of M/s Sharma Traders for March 2025:

- Mar 1: Cash in hand ₹ 8,000; Bank balance ₹ 12,000

- Mar 3: Received cheque from Rajesh ₹ 5,000 and deposited into bank

- Mar 5: Cash sales ₹ 4,000

- Mar 8: Purchased goods for cash ₹ 3,500

- Mar 10: Deposited cash into bank ₹ 2,000 (Contra)

- Mar 12: Paid rent by cheque ₹ 1,500

- Mar 15: Withdrew cash from bank for office use ₹ 1,000 (Contra)

- Mar 18: Cash purchases ₹ 2,200

- Mar 20: Received cash from Suresh ₹ 3,000

- Mar 25: Paid salary by cheque ₹ 2,500

Solution:

| Date | Particulars | L.F. | Cash (₹) | Bank (₹) | Date | Particulars | L.F. | Cash (₹) | Bank (₹) |

|---|---|---|---|---|---|---|---|---|---|

| Mar 1 | To Balance b/d | 8,000 | 12,000 | Mar 8 | By Purchases A/c | 3,500 | – | ||

| Mar 3 | To Rajesh | – | 5,000 | Mar 10 | By Bank A/c | C | 2,000 | – | |

| Mar 5 | To Sales A/c | 4,000 | – | Mar 12 | By Rent A/c | – | 1,500 | ||

| Mar 10 | To Cash A/c | C | – | 2,000 | Mar 15 | By Cash A/c | C | – | 1,000 |

| Mar 15 | To Bank A/c | C | 1,000 | – | Mar 18 | By Purchases A/c | 2,200 | – | |

| Mar 20 | To Suresh | 3,000 | – | Mar 25 | By Salaries A/c | – | 2,500 | ||

| Mar 31 | By Balance c/d | 8,300 | 14,000 | ||||||

| Total | 16,000 | 19,000 | Total | 16,000 | 19,000 | ||||

| Apr 1 | To Balance b/d | 8,300 | 14,000 |

Explanation:

- Contra entries on Mar 10 and Mar 15 are marked C.

- Cash balance = ₹ 8,300; Bank balance = ₹ 14,000.

4.3 Triple Column Cash Book

The Triple Column Cash Book has three amount columns on each side: Cash, Bank, and Discount.

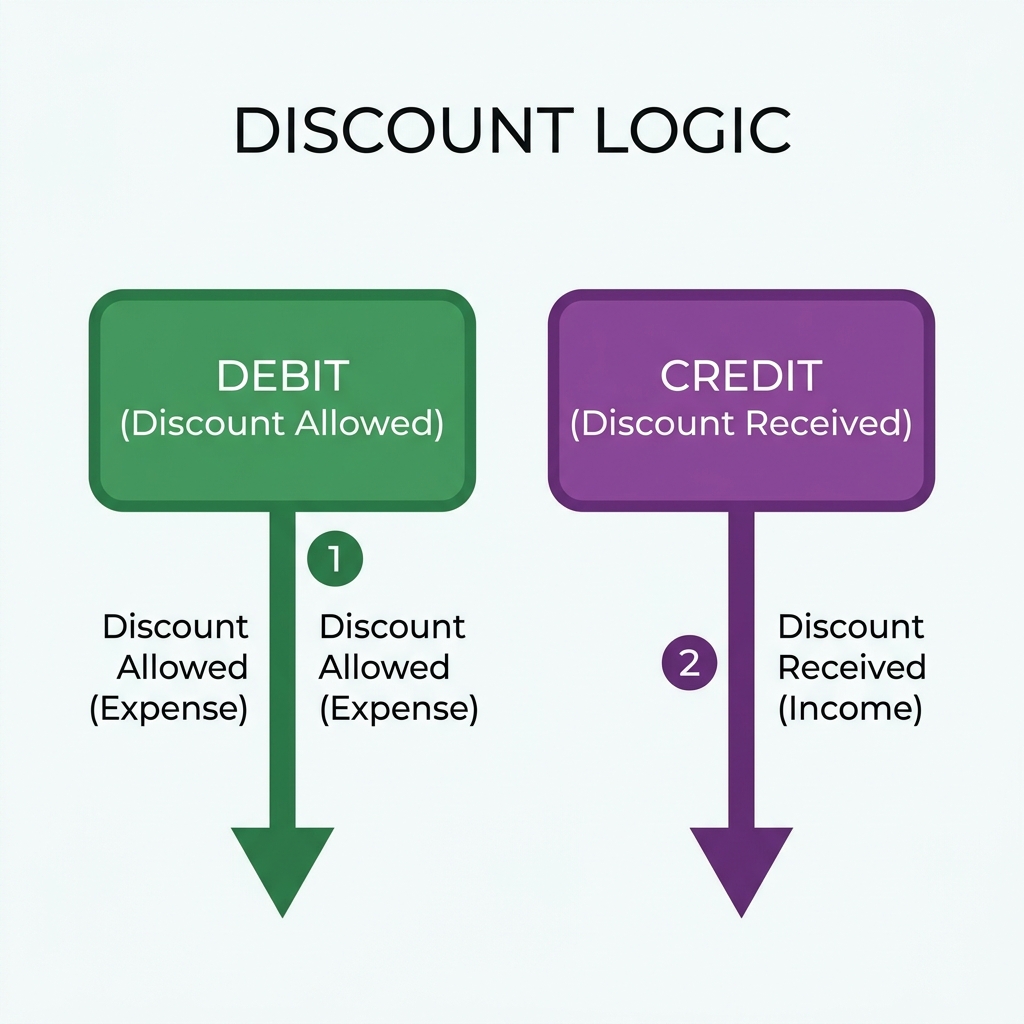

- Discount Allowed (expense) is recorded in the Discount column on the debit side.

- Discount Received (income) is recorded in the Discount column on the credit side.

- The discount columns are memorandum columns – they are not part of double entry. Periodic totals are posted to Discount Allowed A/c (Dr.) and Discount Received A/c (Cr.).

Format:

| Date | Particulars | L.F. | Disc (₹) | Cash (₹) | Bank (₹) | Date | Particulars | L.F. | Disc (₹) | Cash (₹) | Bank (₹) |

|---|---|---|---|---|---|---|---|---|---|---|---|

| To Balance b/d | xxx | xxx | By ………. | xxx | xxx | ||||||

| To ………. | xxx | xxx | xxx | By ………. | xxx | xxx | xxx | ||||

| By Balance c/d | xxx | xxx | |||||||||

| Total | xxx | xxx | xxx | Total | xxx | xxx | xxx |

Illustration (Triple Column Cash Book)

Problem: Enter the following transactions in a Triple Column Cash Book of Mr. Gupta for April 2025:

- Apr 1: Cash in hand ₹ 10,000; Bank balance ₹ 8,000

- Apr 3: Received from Ajay ₹ 4,000; allowed discount ₹ 200

- Apr 5: Paid to Vijay ₹ 2,500; received discount ₹ 100

- Apr 8: Deposited cash into bank ₹ 3,000 (Contra)

- Apr 10: Withdrew from bank for office use ₹ 1,200 (Contra)

- Apr 15: Purchased goods for cash ₹ 2,500

- Apr 18: Received cheque from Kapil ₹ 3,600; allowed discount ₹ 150; cheque deposited into bank

- Apr 22: Paid salaries by cheque ₹ 2,000

- Apr 25: Withdrew from bank for personal use ₹ 800

- Apr 28: Sold goods for cash ₹ 3,500

- Apr 30: Paid rent by cheque ₹ 1,000

Solution:

| Date | Particulars | L.F. | Disc (₹) | Cash (₹) | Bank (₹) | Date | Particulars | L.F. | Disc (₹) | Cash (₹) | Bank (₹) |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Apr 1 | To Balance b/d | 10,000 | 8,000 | Apr 5 | By Vijay | 100 | – | – | |||

| Apr 3 | To Ajay | 200 | 4,000 | – | Apr 5 | By Cash A/c | C | 2,500 | |||

| Apr 8 | To Cash A/c | C | – | 3,000 | Apr 8 | By Bank A/c | C | 3,000 | – | ||

| Apr 10 | To Bank A/c | C | 1,200 | – | Apr 10 | By Cash A/c | C | – | 1,200 | ||

| Apr 18 | To Kapil | 150 | – | 3,600 | Apr 15 | By Purchases A/c | 2,500 | – | |||

| Apr 28 | To Sales A/c | 3,500 | – | Apr 22 | By Salaries A/c | – | 2,000 | ||||

| Apr 25 | By Drawings A/c | 800 | – | ||||||||

| Apr 30 | By Rent A/c | – | 1,000 | ||||||||

| Apr 30 | By Balance c/d | 8,400 | 9,900 | ||||||||

| Total | 350 | 18,700 | 14,600 | Total | 100 | 18,700 | 14,600 | ||||

| May 1 | To Balance b/d | 8,400 | 9,900 |

Explanation:

- Discount columns are totalled: Discount Allowed = ₹ 350; Discount Received = ₹ 100.

- Contra entries (Apr 8, Apr 10) are marked C.

- Cash balance = ₹ 8,400; Bank balance = ₹ 9,900.

4.4 Petty Cash Book

To avoid overloading the main Cash Book with numerous small payments (e.g., postage, stationery, tea, carriage, etc.), a Petty Cash Book is maintained by a petty cashier.

Imprest System

- The petty cashier is given a fixed amount (the imprest), say ₹ 2,000.

- At the end of the period, the total payments are calculated.

- The main cashier reimburses the petty cashier with the amount spent, restoring the imprest to the original fixed amount.

Format (Analytical Petty Cash Book):

| Date | Particulars | Voucher No. | Total Payment (₹) | Postage (₹) | Stationery (₹) | Conveyance (₹) | Tea & Refreshments (₹) | … etc. |

|---|

Posting from Petty Cash Book:

- Total of each expense column is posted to the debit of the respective expense account.

- Total payments are credited to the main Cash Account when reimbursed.

Illustration (Petty Cash Book – Imprest System)

Problem: The petty cashier was given an imprest of ₹ 2,000 on April 1. Payments made:

- Apr 3: Postage ₹ 150

- Apr 5: Stationery ₹ 200

- Apr 8: Conveyance ₹ 80

- Apr 12: Tea & Refreshments ₹ 100

- Apr 15: Postage ₹ 120

- Apr 18: Stationery ₹ 150

- Apr 22: Conveyance ₹ 90

- Apr 25: Tea & Refreshments ₹ 80

- Apr 28: Postage ₹ 100

- Apr 30: Stationery ₹ 120

Solution (Analytical Petty Cash Book):

| Date | Particulars | Voucher No. | Total | Postage | Stationery | Conveyance | Refreshments |

|---|---|---|---|---|---|---|---|

| Apr 1 | To Cash A/c (Imprest) | (2,000) | |||||

| Apr 3 | Postage | 1 | 150 | 150 | |||

| Apr 5 | Stationery | 2 | 200 | 200 | |||

| Apr 8 | Conveyance | 3 | 80 | 80 | |||

| Apr 12 | Tea & Refreshments | 4 | 100 | 100 | |||

| Apr 15 | Postage | 5 | 120 | 120 | |||

| Apr 18 | Stationery | 6 | 150 | 150 | |||

| Apr 22 | Conveyance | 7 | 90 | 90 | |||

| Apr 25 | Tea & Refreshments | 8 | 80 | 80 | |||

| Apr 28 | Postage | 9 | 100 | 100 | |||

| Apr 30 | Stationery | 10 | 120 | 120 | |||

| Total | 1,190 | 370 | 470 | 170 | 180 | ||

| Apr 30 | By Balance c/d | 810 | |||||

| May 1 | To Cash A/c (Restored) | 1,190 |

Analysis:

- Total payments during April = ₹ 1,190.

- Petty cash in hand = ₹ 810.

- On May 1, the petty cashier receives ₹ 1,190 to restore the imprest to ₹ 2,000.

5. Summary Table of Cash Book Types

| Type | Columns | Purpose | Best For |

|---|---|---|---|

| Single Column | Cash | Only cash receipts & payments | Small businesses with no bank account |

| Double Column | Cash + Bank | Cash and bank transactions | Businesses with a bank account but few discounts |

| Triple Column | Cash + Bank + Discount | Cash, bank, and cash discounts | Businesses that frequently give/receive discounts |

| Petty Cash | Analytical columns | Small routine expenses | All businesses to reduce main cash book load |

6. Key Points to Remember

- Contra Entry: Affects both cash and bank; marked with ‘C’; no further posting.

- Discount Columns: Not part of double entry; totals posted to Discount Allowed and Discount Received accounts.

- Balancing: Cash column always shows a debit balance. Bank column can show debit (favourable) or credit (overdraft) balance.

- Petty Cash: Usually maintained under the Imprest System to maintain control.

7. Practice Problems

Problem 1 (Double Column Cash Book)

Enter the following transactions in a Double Column Cash Book (Cash & Bank) of Mr. Verma for May 2025:

- May 1: Cash in hand ₹ 6,000; Bank balance ₹ 10,000

- May 3: Received cheque from Anil ₹ 4,500 and deposited into bank

- May 5: Cash sales ₹ 3,200

- May 7: Paid to Sunil by cheque ₹ 2,800

- May 10: Deposited cash into bank ₹ 2,000 (Contra)

- May 12: Purchased goods for cash ₹ 1,500

- May 15: Withdrew cash from bank for office use ₹ 1,200 (Contra)

- May 18: Received cash from Rohit ₹ 2,000

- May 20: Paid salary by cheque ₹ 3,000

- May 25: Paid rent in cash ₹ 800

- May 28: Sold goods and received cheque ₹ 3,000, deposited into bank

Problem 2 (Triple Column Cash Book)

Prepare a Triple Column Cash Book from the following transactions:

- Jan 1: Cash in hand ₹ 12,000; Bank balance ₹ 8,000 (overdraft)

- Jan 3: Received from Brijesh ₹ 5,000; allowed discount ₹ 250

- Jan 5: Paid to Rahul ₹ 3,000; received discount ₹ 150

- Jan 8: Deposited cash into bank ₹ 4,000 (Contra)

- Jan 10: Withdrew from bank for office use ₹ 2,000 (Contra)

- Jan 12: Cash sales ₹ 3,500

- Jan 15: Paid wages by cheque ₹ 1,800

- Jan 18: Received cheque from Anita ₹ 4,200; allowed discount ₹ 200; cheque deposited

- Jan 22: Paid electricity bill by cash ₹ 500

- Jan 25: Withdrew from bank for personal use ₹ 1,000

- Jan 28: Cash purchases ₹ 2,200

- Jan 30: Paid insurance by cheque ₹ 1,500

Problem 3 (Petty Cash Book)

Prepare an Analytical Petty Cash Book under the Imprest System with columns: Postage, Stationery, Conveyance, and Miscellaneous. Imprest is ₹ 1,500.

- Jan 1: Received imprest

- Jan 3: Postage ₹ 80, Jan 5: Stationery ₹ 120, Jan 8: Conveyance ₹ 60, Jan 10: Misc ₹ 50

- Jan 12: Postage ₹ 70, Jan 15: Stationery ₹ 90, Jan 18: Conveyance ₹ 80, Jan 20: Misc ₹ 40

- Jan 22: Postage ₹ 60, Jan 25: Stationery ₹ 100, Jan 28: Conveyance ₹ 50, Jan 30: Misc ₹ 30

Practice MCQs

[!TIP]

Master the concepts of Subsidiary Books and Cash Book with 30 custom MCQs designed for competitive exams.